Deep Tech: Clearing Up Misconceptions

Rethinking capital, timeline, risk, and returns at the frontier

We are a tech generalist fund: we invest across categories, mostly in software. But we also deliberately invest in deep tech, especially in health tech (Raidium, OneBioScience, Dune), tech bio (Oria Bioscience, Generare), agtech (.omics, EPICS Biotechnology, etc.) and other critical technologies (Vaire and a stealth companies in industries like defence). Sometimes people ask why we wander into what are seen as disputable territories. The answer is simple: these areas are not tangents, they are the original ground of venture capital, and done well, they are among the most rewarding bets in the industry. (And as a side note, if Europe is serious about sovereignty and long-term value creation, they are indispensable.)

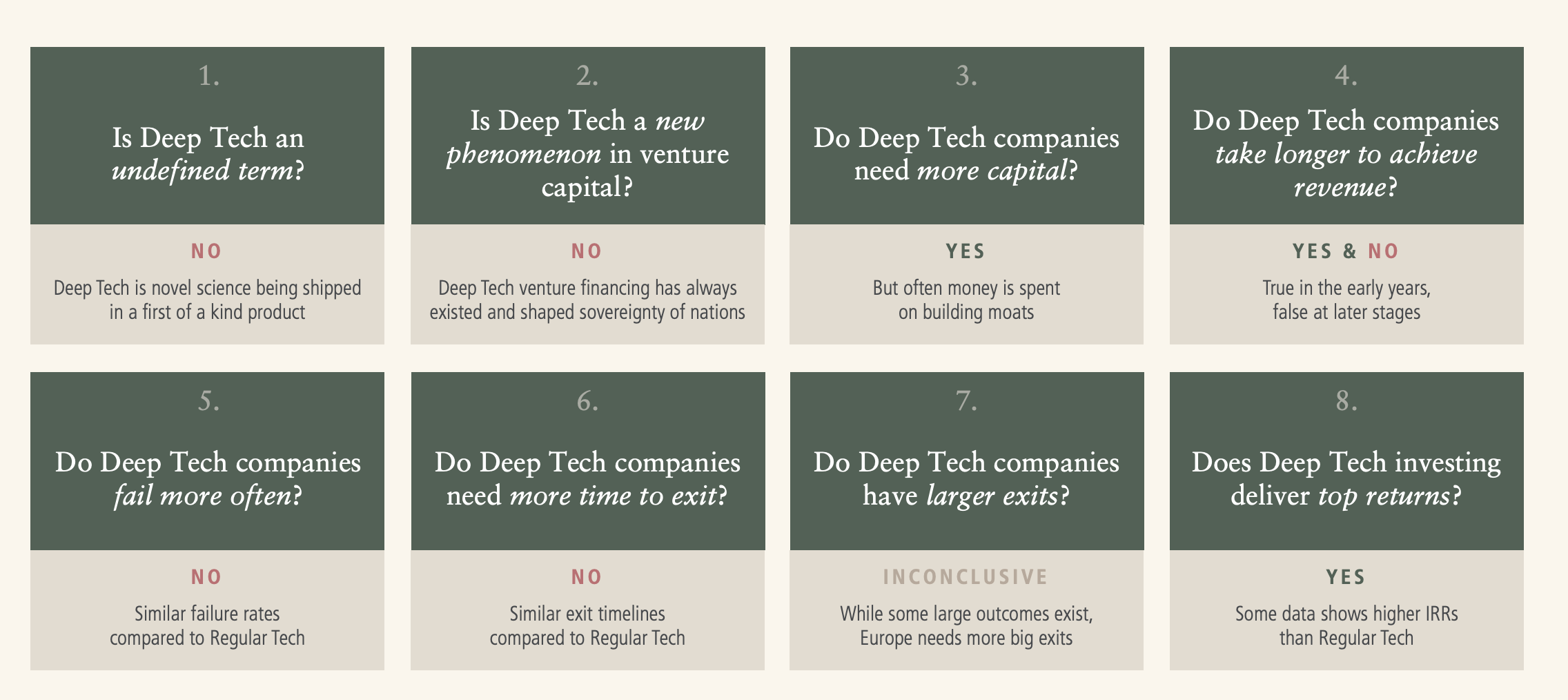

The 2025 European Deep Tech Report, released last March by Lakestar, Walden Catalyst & Dealroom highlights a persistent problem: deep tech is often misunderstood.

Defined as novel scientific or engineering breakthroughs shipped in first-of-a-kind products, deep tech is frequently framed through misconceptions that distort how capital is allocated.

The first part of the report, dedicated to these misconceptions, is especially insightful, because it surfaces generalised beliefs that are deeply detrimental to the industry, and to the asset class financing it.

Misconceptions are not harmless. They don’t just distort public narratives; they redirect investment away from frontier opportunities, and slow or even prevent the emergence of industries critical to Europe’s future.

Let me focus on a few critical points, and add my own perspective:

“It’s a hype and VC should avoid doing it.”

From the very beginning of modern venture capital in the mid-20th century, capital has been directed toward scientific and engineering breakthroughs that promised to reshape economies and geopolitics:

Historical waves of sovereignty & value creation

Each technological wave has defined not only industries but also national power:

Internal combustion engines and chemicals anchored German industrial strength.

Electricity and aviation helped the US build economic and military dominance.

Petrochemicals positioned the Middle East as a geopolitical force.

Electronics and semiconductors created Japan’s rise in the 70s–80s, then Taiwan and South Korea.

Software and digital networks gave the US (and increasingly China) global control over platforms, data, and standards.

And venture capital has always been entangled with these waves:

1940s-1970s: VC is born in the post-war years to finance semiconductors, defence, aerospace (following state de-risking from DARPA and NASA). Carlota Perez’s framework helps read the pattern: installation (capital floods in, bubbles form) → turning point (restructuring) → deployment (wide diffusion). Perez reminds us that bubbles are not bugs but features of installation: they overfund exploration and create the raw material for deployment. From DARPA to NASA to the EU Chips Act, the public sector has always intentionally (over)funded early exploration to build scaffolding. Venture capital cannot pull the installation phase alone, but it accelerates the match between supply and demand for innovation, shaping markets around frontier technologies.

1970s–2020: VC adapted to software’s fast cycles and low CAPEX. But that was the exception, not the rule. The original DNA of venture has always been deep tech: nonlinear, infrastructure-heavy.

Today’s bets: computational biology (health & agtech), defence, new materials, energy, space, robotics, are closer to the root of venture capital than pure SaaS ever was. And the good news: while plenty of SaaS-ified AI will proliferate, the gravitational pull of CAPEX-intensive AI models and ever-evolving architectures ensures that the most defensible value will emerge in hard tech, where science and uncertainty define the frontier (and maximise value creation).

“Deep Tech companies burn too much capital and fail more often.“

It is true that many deep tech ventures require significant upfront investment. But, capital intensity ≠ capital inefficiency. In aerospace, semiconductors, or biotech, breakthrough outcomes have typically required high burn, not as a guarantee of success, but as the price of entry to build defensibility and capture outsized payoffs. Tesla, Moderna, and SpaceX all absorbed billions before proving sustainable models. The lesson is not that they burned “too much,” but that transformative industries demand deep reservoirs of risk capital before they compound into dominant positions. Yes, deep tech raises larger rounds, but that capital goes into infrastructure and IP, not inflated ad budgets feeding GAFAMs. What matters is not burn, but what the burn builds: IP, standards, and manufacturing muscle that persist long after early capital is spent.

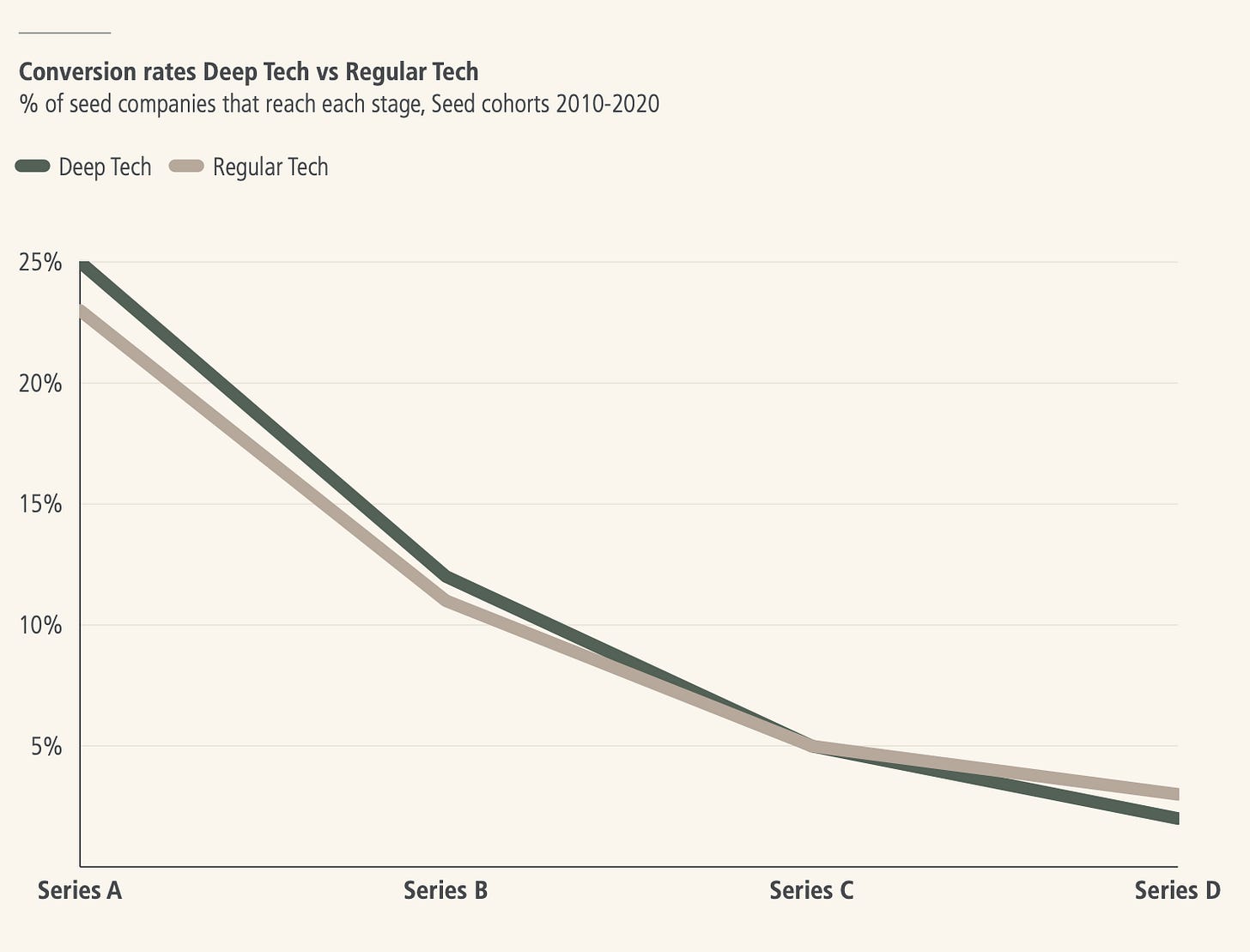

The failure narrative is equally misleading. The denominator problem is often ignored: most software startups also fail, but they do so quickly and invisibly, producing a survivorship bias in venture narratives. Deep tech failures are simply more visible because they are fewer in number, larger in scale, and often linked to state or corporate partnerships, not because they are statistically more common. When normalised for stage, failure rates are not materially different from other tech.”

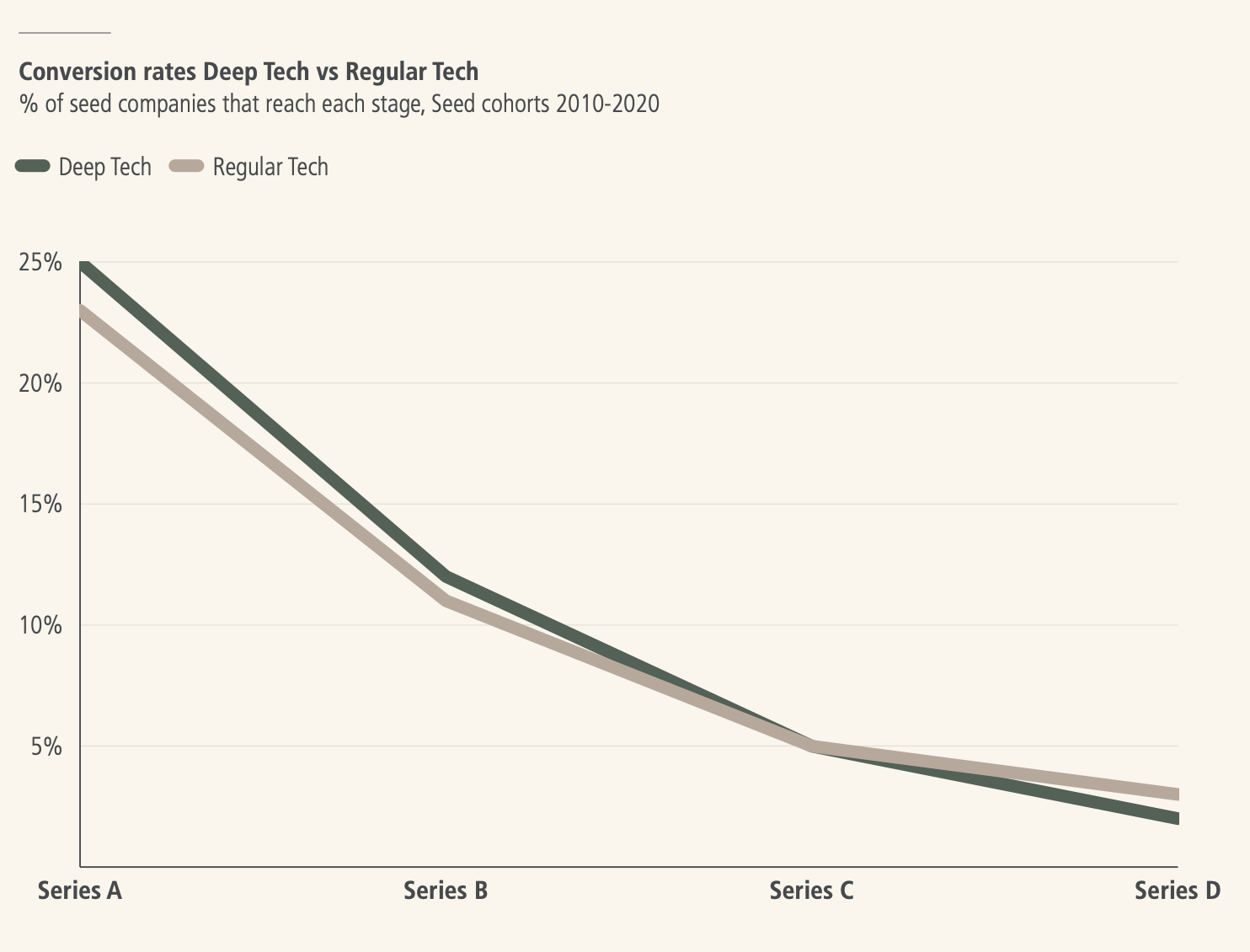

Conversion rates (seed → A → D) show no meaningful difference between deep tech and regular tech (both drop from ~25% at seed to <5% at D). This directly disproves the “fail more often” narrative. “Deep Tech takes more time, from revenue to exits.”

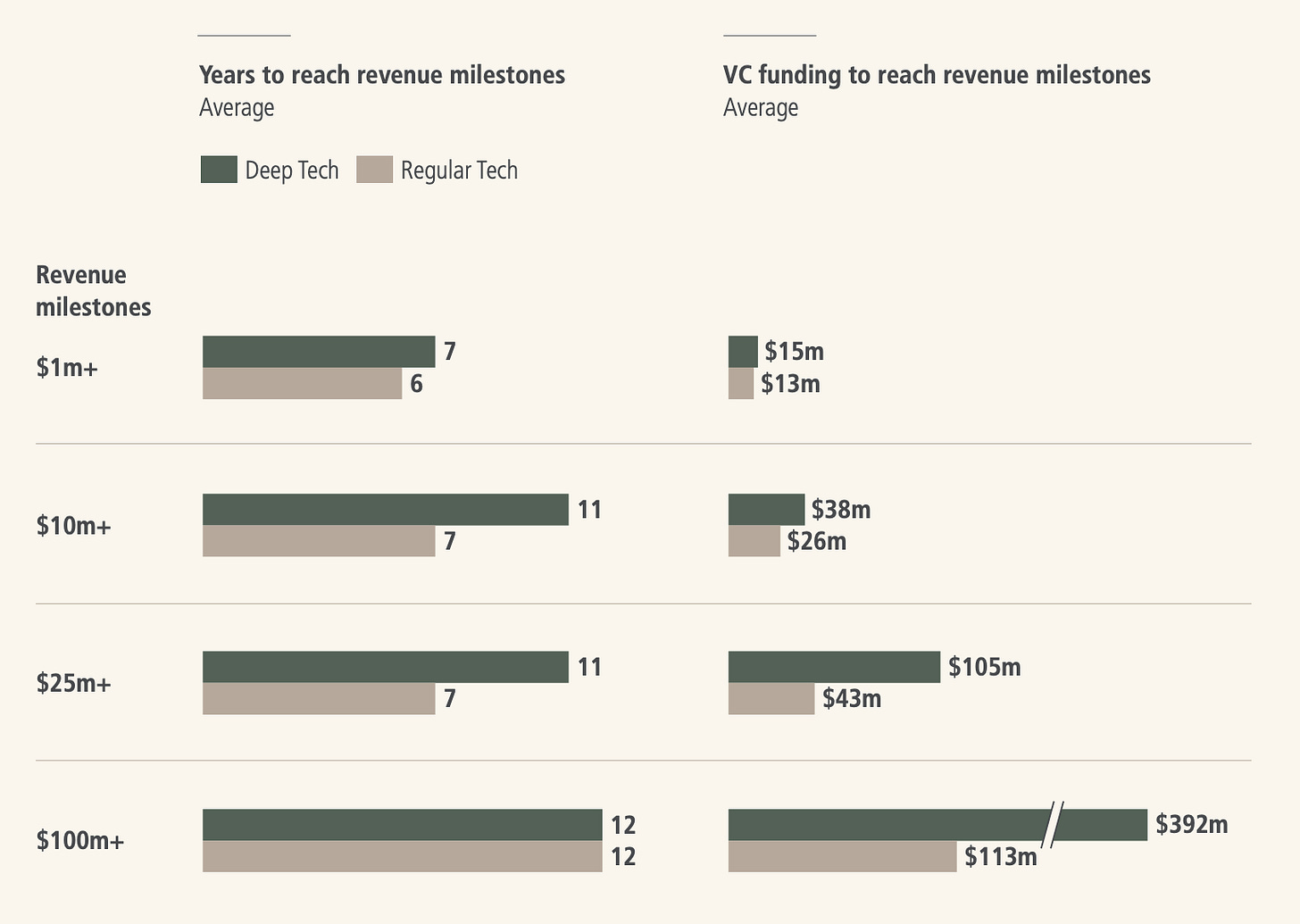

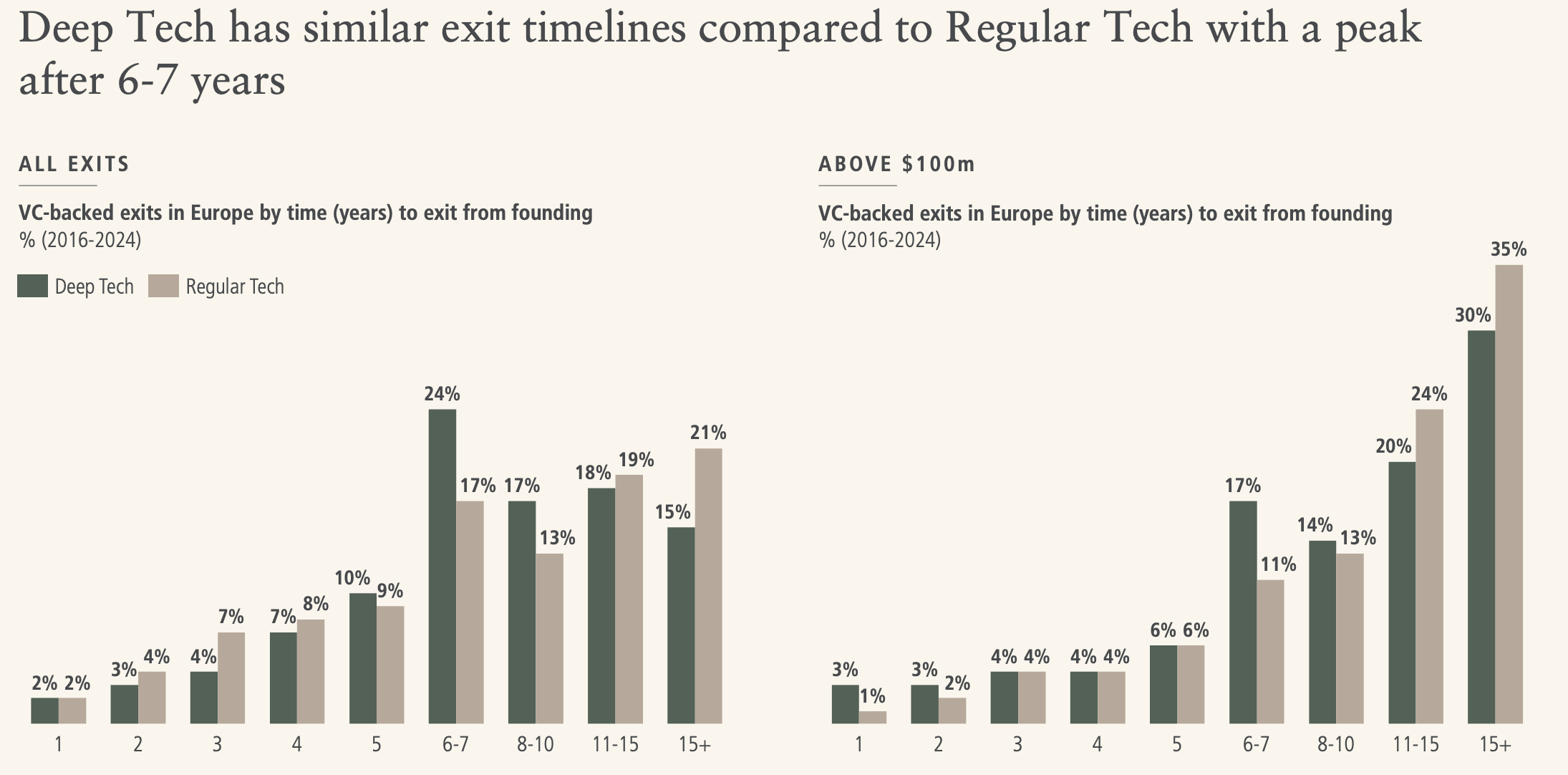

This critique often confuses time-to-revenue with time-to-value. Deep tech often does take longer to commercialise, but its impact, once de-risked tends to be systemic and sticky. Contrast a SaaS workflow tool that can be displaced in 18 months (the fear haunting many 2010s SaaS companies facing AI)) with a novel technology that decodes decodes tumor signatures to guide treatment decisions. Vertical software chase quick logos and ARR (and nothing wrong with that, with the right positioning and speed of execution); deep tech cycles reshape supply chains, which, once locked, endure for decades

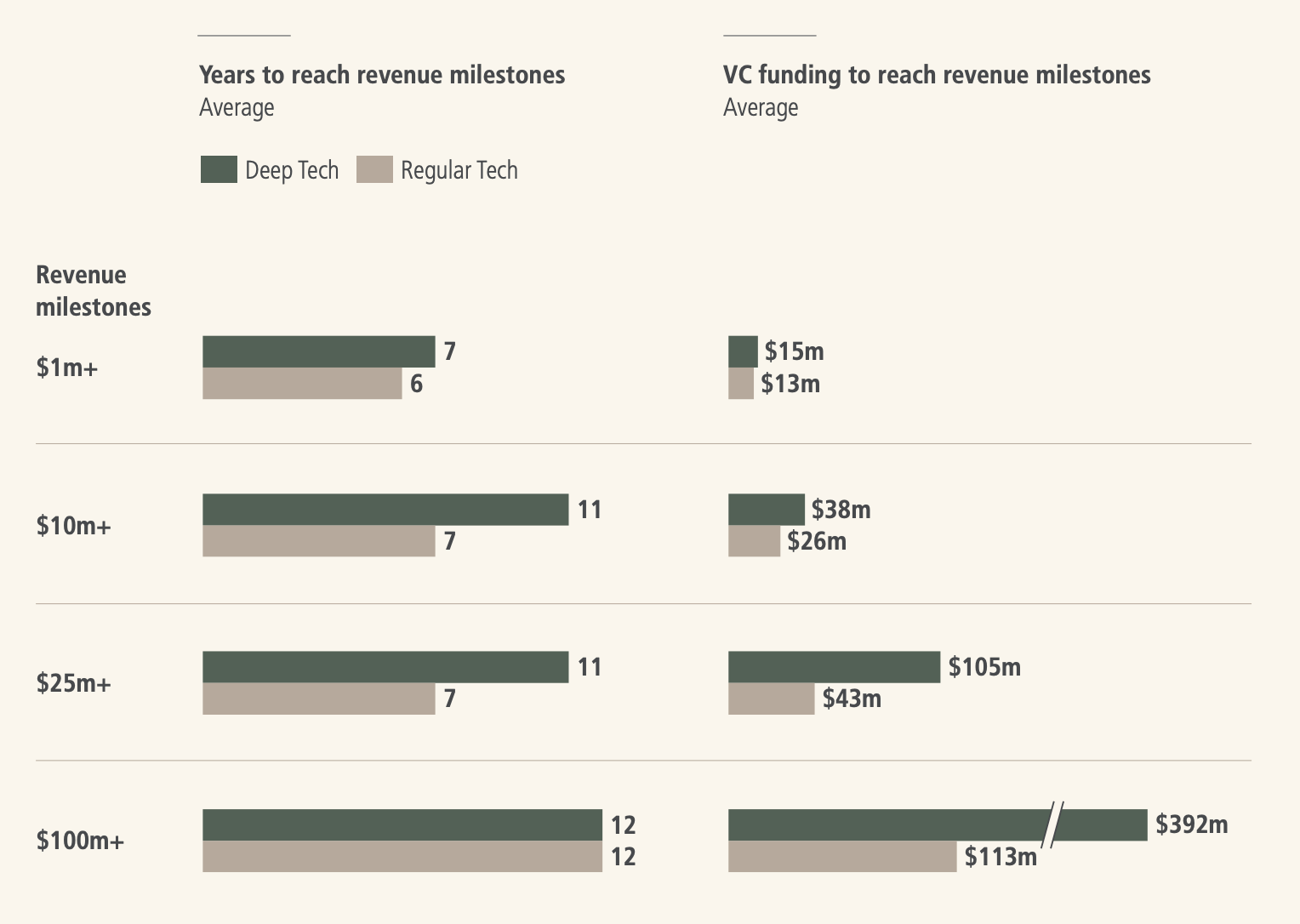

Deep tech lags in the $10m–$25m phase, but once scaling inflects, convergence is real: $100m ARR is reached in the same 12 years as regular tech, with far deeper barriers to entry.

Left: Time to $1m revenue: only 1 year longer (7 vs 6). Time to $100m revenue: identical (12 years). This undermines the “too slow” claim. Right: Funding to milestones: deep tech needs more at $25m+ revenue ($105m vs $43m), but not exponentially more, and burn translates into durable infrastructure. Carlota Perez shows that bubbles and apparent slowness in the installation phase are not wasted time, they build the infrastructures for deployment. At the venture level, what looks like a long path to revenue in deep tech is often the same phenomenon in miniature: incubation that creates technologies and ecosystems which, once they diffuse, are more resilient than software cycles.

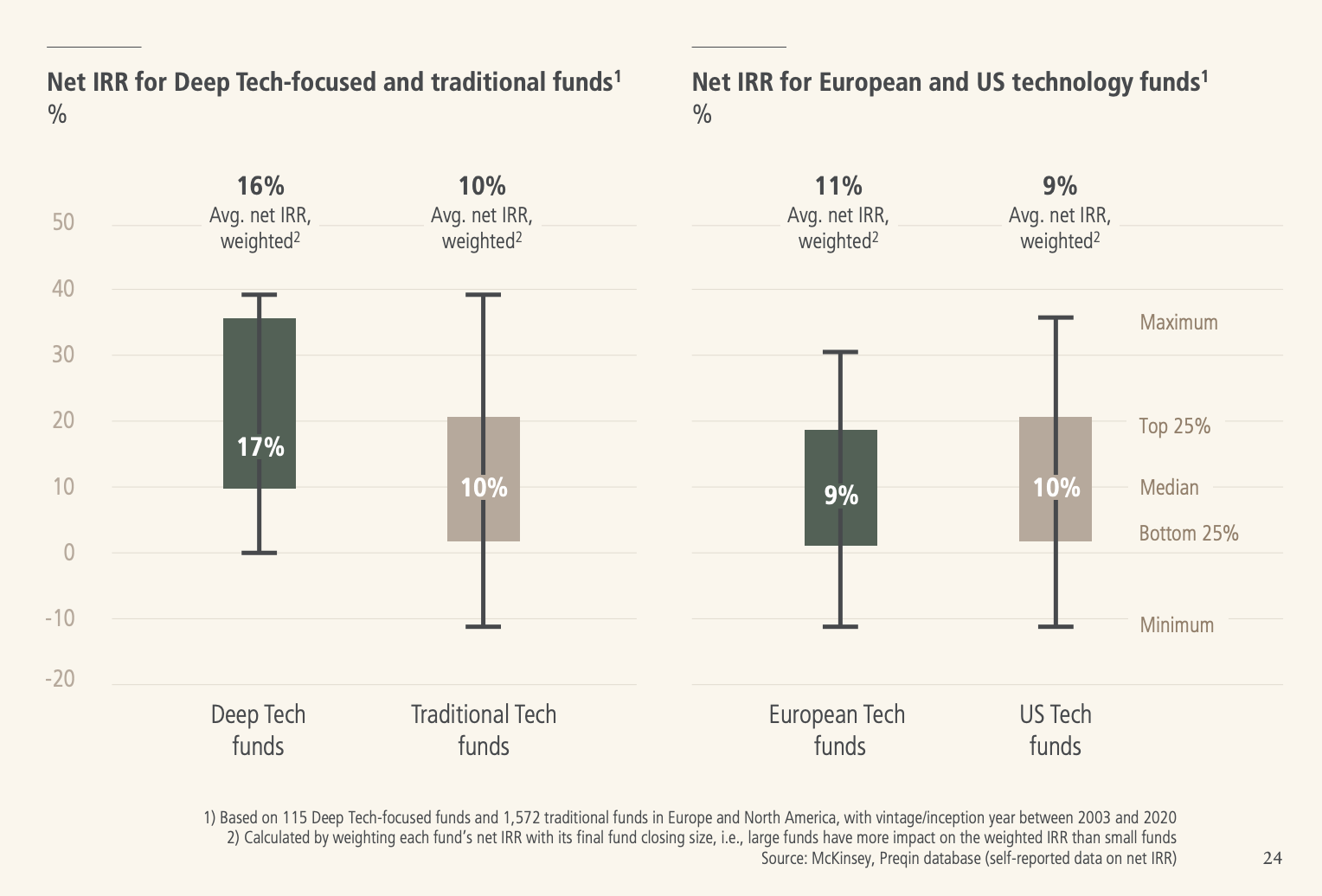

“Returns aren’t there.”

Historical data contradicts this misconception. Biotech alone accounts for a disproportionate share of venture-backed IPOs and acquisitions in the last 30 years. Semiconductors, life sciences, and energy have consistently produced dragon outcomes (companies that return entire funds), despite high volatility (inherent to venture capital).

What obscures this truth is the way venture metrics are aggregated: software has dominated because of sheer volume, not because deep tech underperforms. In fact, in a power law industry such as venture capital, it only takes one or two companies to generate portfolio multiple. It’s even more pronounced in deep tech: Nvidia, Tesla, and Moderna were all capital-intensive, long-cycle bets once dismissed as ‘too hard’ or ‘too slow.

Deeptech companies are harder to analyse, require more patience, and often depend on stronger alignment with state and industrial partners… But when they work, they reshape industries and deliver outcomes beyond what narrow SaaS multiples can ever achieve.

Deep tech doesn’t fail more often, doesn’t waste capital, doesn’t take longer, and does deliver returns. The real question is whether European venture will align capital with this reality.

A resilient venture portfolio should balance risks across industries, so we will continue investing in software, which can generate outsized outcomes.

But we are equally convinced that many European strategic frontiers, and much of tomorrow’s value creation, lies in deep tech.

PS: you can find the entire report here and a TL;DR summary of the misconceptions chapter below.